MWC 2026 trends: agentic AI, AI-native 6G and the future of cognitive telecoms

The Mobile World Congress (MWC) 2026 in Barcelona confirmed a crucial shift from the "buzz" surrounding generative AI to its practical, deep integration across telecommunications infrastructure. The primary focus of the event was Agentic AI and the acceleration towards AI-Native 6G networks, promising to fundamentally transform the industry's operational technology. Our team attended MWC, sharing some of the key trends and insights that emerged from the event.

Agentic AI and AI-driven BSS/OSS

Messaging from BSS/OSS (business and operational support systems) vendors has shifted conclusively from static, rule-based automation to agentic BSS/OSS, where largely autonomous AI agents manage various aspects of customer and network technology. Amdocs, Netcracker, Nokia, and Ericsson heavily promoted the potential of Agentic AI in BSS/OSS workflows while Hansen, Cerillion, and Tecnotree demonstrated capabilities that leverage AI-based technology to drive comprehensive automation.

The ultimate objective is an autonomous platform capable of addressing numerous use cases for telcos without human intervention. This includes critical areas like network management, for example, answering the question: "why is this part of my network suddenly consuming much more power than usual?", and customer care, such as instructing the system to: "respond to this customer support request in chat by fixing their billing issue then upselling them a customised bundle of services, then provisioning it if they say yes," and much more. More than just detecting an issue, Agentic AI guarantees to actually, autonomously take the steps required to resolve it, whether that be through network management or processing an order for, say, an upsold subscription plus CPE (customer premises equipment).

A fully autonomous platform requires fewer personnel to achieve the desired network and business outcomes, theoretically reducing ongoing costs. However, the specialists needed for design, implementation, and monitoring will likely command higher salaries. For the vendors themselves, the embrace of agentic AI BSS/OSS could be a "double-edged sword" given the significant revenues generated from the professional services required to integrate and manage complex BSS/OSS implementations.

The buyers’ perspective

Our discussions with technology decision-makers at both large and small CSPs confirmed that the complexity, time, and resources required for deploying BSS/OSS platforms or modules mean that the yearly influx of sophisticated marketing messaging makes little difference. Buying cycles for BSS/OSS are measured in years, not months. These cycles involve extensive consultative discussions with potential vendors and lengthy evaluation processes, making them very expensive for both the vendor and the buyer. Unless there is a compelling reason to switch, buyers are generally more inclined to engage with their existing supplier for desired changes and new features.

BSS/OSS software is comparable to ERP deployments: they are so profoundly embedded within an organisation, and subsequently customised with specific requirements, workflows, exceptions, and rulesets, that the switching costs are substantial disincentives to change. Opportunities to replace comprehensive single-vendor BSS/OSS deployments are limited, and those that do arise will be time-consuming and costly to realise.

There is arguably greater potential to compete for sections of the stack using "best-of-breed" modules accessed through open APIs. For new entrants into the network operator business, the benefit is clearer, allowing greenfield operations to achieve high levels of customer and network experience rapidly without the inherent complexities that BSS/OSS implementations typically demand.

Intelligent home hubs: the future of broadband CPE

Broadband CPE (customer premises equipment) is evolving beyond a simple “connectivity box”. It is transitioning into an intelligent home hub that integrates a wide range of additional capabilities around connectivity, specifically focusing on smart home functionality, security and entertainment. The dominant trends involve the integration of 5G-advanced (5G-A), Wi-Fi 8 and edge AI.

The four main areas of advancement observed at MWC 2026 were:

- The introduction of Wi-Fi 8 CPE: devices featuring the latest Wi-Fi standard, offering increased speed, efficiency, and reliability for the most demanding home environments.

- AI-Native FWA (fixed wireless access): AI optimises FWA performance and management, establishing it as a robust, highly competitive alternative to fibre.

- The "all-in-one" AI home hub: a functional consolidation where a single device manages connectivity, security, and local AI processing for various smart home devices.

- 50G PON and 5G-advanced integration: This lays the foundation for future-proof, multi-gigabit connections by combining both fixed and wireless access technologies.

It is important to note that post-MWC, adoption of these new technologies is now likely to be slower in the U.S.

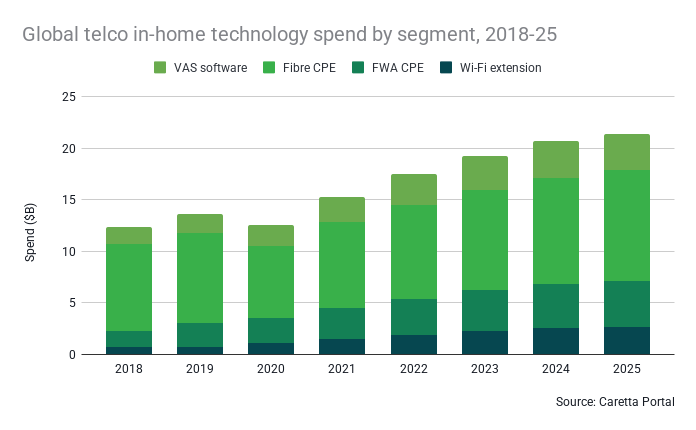

The total market value for fiber and FWA CPE, Wi-Fi extension and VAS software, increased from $12B in 2018 to $21B in 2025, achieving a compound annual growth rate (CAGR) of 8%.

Hardware and consumer updates from MWC 2026

While the core focus was on infrastructure, the consumer hardware ecosystem is also evolving to support this AI-native world. Universal connectivity and satellite-to-cell (NTN) technology have moved into the mainstream. On the device front, the “app-free” concept gained traction through AI-native smartphones and glasses. We also saw advancements in Silicon-Carbon battery technology and tri-fold displays, leading to more power-efficient and versatile form factors, exemplified by new launches like the Samsung Galaxy S26 range and Honor’s “Robot Phone”.

Key strategic takeaways from MWC 2026

Beyond core operations, MWC 2026 solidified several major strategic shifts for the telecoms industry:

- Agentic AI: autonomous AI agents are becoming the standard for network and on-device tasks.

- AI-native 6G: the 6G roadmap is now defined as a "grid for physical AI," with edge processing prioritised over simple data transmission.

- Satellite integration: seamless switching between cellular and LEO satellite networks (NTN) is now the standard goal for global roaming.

- Sovereign AI, infrastructure and networks: a strategic push by global telcos to build regional AI frameworks to ensure data privacy and digital independence, an important focus for data regulation in Europe and beyond.

What MWC 2026 trends mean for vendors

MWC 2026 was a pivotal moment as vendors positioned AI as the foundation of modern telecommunications software. The move to agentic BSS/OSS and intelligent home hubs positions the industry for an era of autonomous operation. For telcos across the United Kingdom and the wider European market, evaluating the competitive impact of adopting AI driven infrastructure is becoming increasingly important.

To learn more about our full telecoms tech market analysis and reports at Caretta Research, contact us at info@carettaresearch.com.

Blog post tags

Blog posts

Read more

July 21, 2026

July 7, 2026

June 11, 2026