Why broadcasters must embrace YouTube now

While traditional broadcasters, studios and premium streaming services were focused on waging the streaming wars, YouTube quietly transitioned from a mobile-first short-form UGC platform to a dominant force in the living room, siphoning off both viewer attention and advertiser dollars previously reserved for broadcast TV. For broadcasters in the UK and Europe, the core strategic challenge is to find the right balance between capitalising on YouTube’s instant audience reach and revenue, and protecting their long-term data autonomy and proprietary “walled garden” platforms.

Why ignoring YouTube is no longer an option

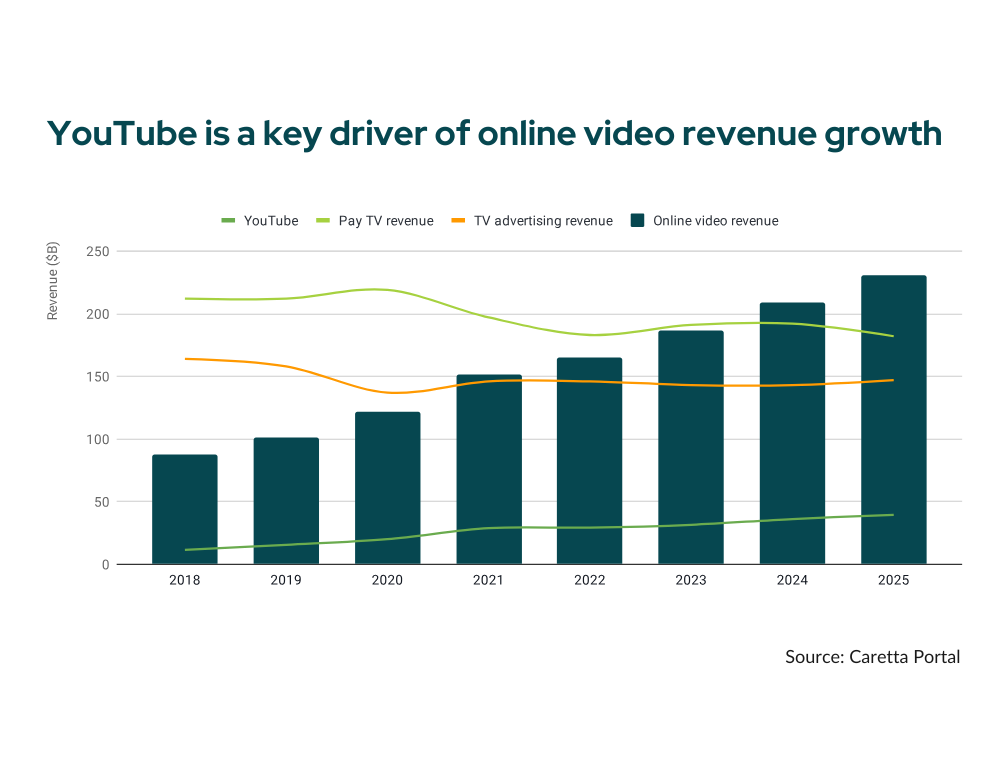

YouTube’s scale is almost difficult to comprehend. With roughly 35 years of content uploaded to the platform every single year, the volume of new content added to YouTube annually is now 25 times larger than all professional content produced globally.

Beyond its size, YouTube’s ability to monetise its scale is unparalleled, capturing approximately 17% of total online video revenue, which is also equivalent to roughly one-third of the global traditional TV advertising market. While professional content as a category still commands greater viewing time and revenue in aggregate, YouTube has effectively surpassed every individual broadcaster and video service. Crucially, YouTube is now emerging as a dominant force in CTV: as of 2024, television has already replaced mobile as the leading device for viewing YouTube in the US. As this trend expands globally, it is no longer a question of if a broadcaster should be there, but how.

Download the full presentation from the Future of TV Advertising Global, here.

The YouTube spectrum: three engagement models for broadcasters

When engaging with YouTube, broadcasters pick an approach that fits their specific business goals and how much risk they are willing to take.

- The teaser channel: YouTube acts strictly as a marketing vehicle. Broadcasters or streamers like Netflix upload short clips and trailers designed to build "fandom" and funnel viewers back to their owned-and-operated (O&O) platforms.

- Thoughtful engagement: broadcasters recognise that specific demographics, particularly younger audiences, may only consume their content on YouTube. They curate or even create dedicated content specifically for the platform to meet these viewers where they are, while still keeping their primary business operations elsewhere.

- Premium curation: broadcasters treat YouTube as a primary destination equivalent to their own TV channels. They curate premium, brand-safe environments on the platform and take full control of ad sales via the Google Ad Manager partner sales program.

This spectrum is fluid, but not path dependent. As demonstrated by NBC’s approach to the Olympics (using influencers to build hype while retaining core viewing on their own platforms) demonstrates that the "middle ground" can be a highly effective, permanent strategic choice rather than a transition phase.

Download the full presentation from the Future of TV Advertising Global, here.

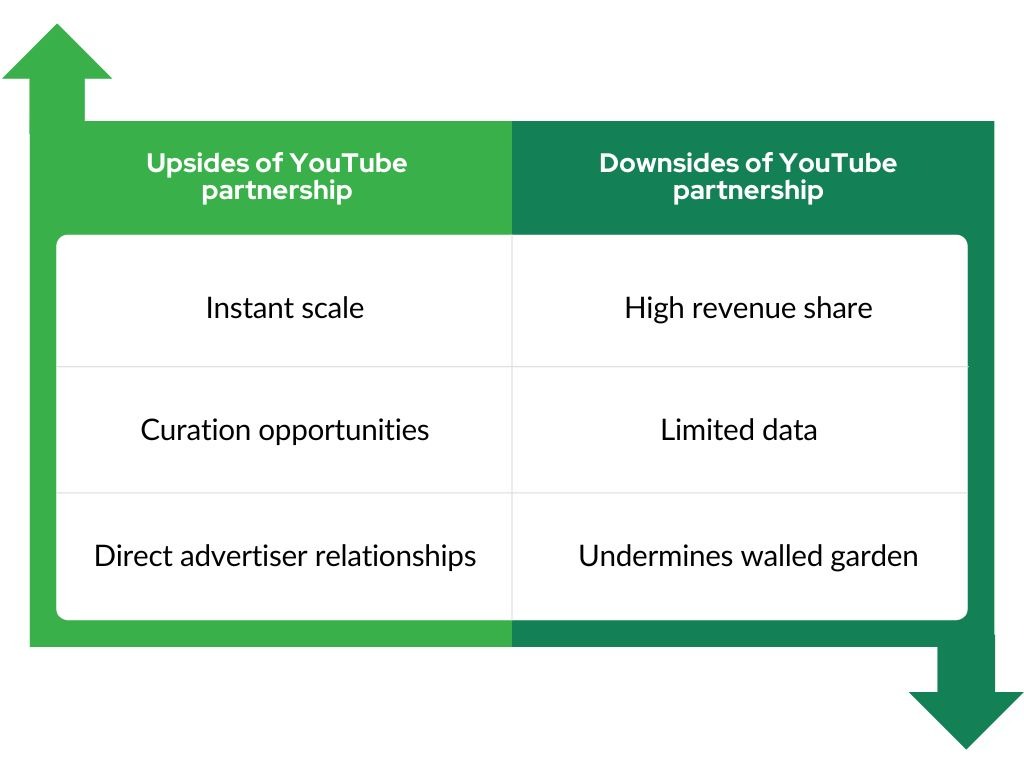

Broadcaster strategy trade-offs: upsides and downsides of relying on YouTube

The move toward deeper YouTube engagement is a double-edged sword, offering immediate tactical gains at the expense of long-term structural control.

Upsides of YouTube partnership:

- Instant audience reach and revenue: broadcasters gain immediate access to a massive audience and instant revenue, bypassing the lengthy and costly build-out of a proprietary ad technology backend.

- Curated brand-safe environments: The ability to ring-fence their premium content channels, offering advertisers a high-quality, controlled environment despite the uncontrolled surrounding open marketplace.

- Direct advertiser relationships: They maintain control over campaign management and can integrate YouTube into "total audience buys" at the deal-making level, preserving their relationship with ad buyers.

Downsides of YouTube partnership:

- High revenue share: the standard creator revenue split is often 45/55 in YouTube's favour, though major broadcasters have negotiation power for their premium content.

- Loss of data and control: YouTube retains full control of the platform and its data. Broadcasters receive limited visibility beyond aggregate reporting and cannot integrate their YouTube business into their own first-party data platforms or self-serve tools.

- Undermining proprietary platform: deep engagement fundamentally works against the broadcaster’s core objective to build a proprietary walled garden, a platform where they control the audience, the technology and the advertising data. The model is structurally designed for the individual content creator (like MrBeast or Ryan’s World), not the legacy media organisation.

Download the full presentation from the Future of TV Advertising Global, here.

Key takeaway: strategy over dependency in the streaming wars

The transition to a streaming-first business is not a guaranteed success. Not every broadcaster has the resources to become a "walled garden" on their own. This is evidenced by the pivot of powerhouses like Sony Pictures and Lionsgate toward a wholesaler model, and the rise of consortiums like Joyn or Freely, which seek strength in numbers.

Furthermore, for many European broadcasters, these commercial trade-offs are complicated by a public service mandate. The duty to inform and reach the entire population often sits in direct tension with the desire to lock content behind a proprietary, data-rich ecosystem.

As the industry consolidates, the most successful broadcasters will be those who recognise that a "walled garden" isn't the only path to survival. The real victory lies in making a deliberate choice: finding the right balance between the instant reach of global platforms and the hard-won autonomy of their own technology.

For more information on broadcasters’ distribution and monetisation strategies or other insights into ad tech, you can download the full presentation from the Future of TV Advertising Global, or contact us at info@carettaresearch.com.

Blog post tags

Blog posts

Read more

July 21, 2026

July 7, 2026

June 10, 2026